If you have ever opened a budgeting app, stared at 30 empty categories, and closed it immediately — you are not alone. The 50/30/20 rule exists precisely for that moment. It is the antidote to over-complicated budgeting.

What Is the 50/30/20 Rule?

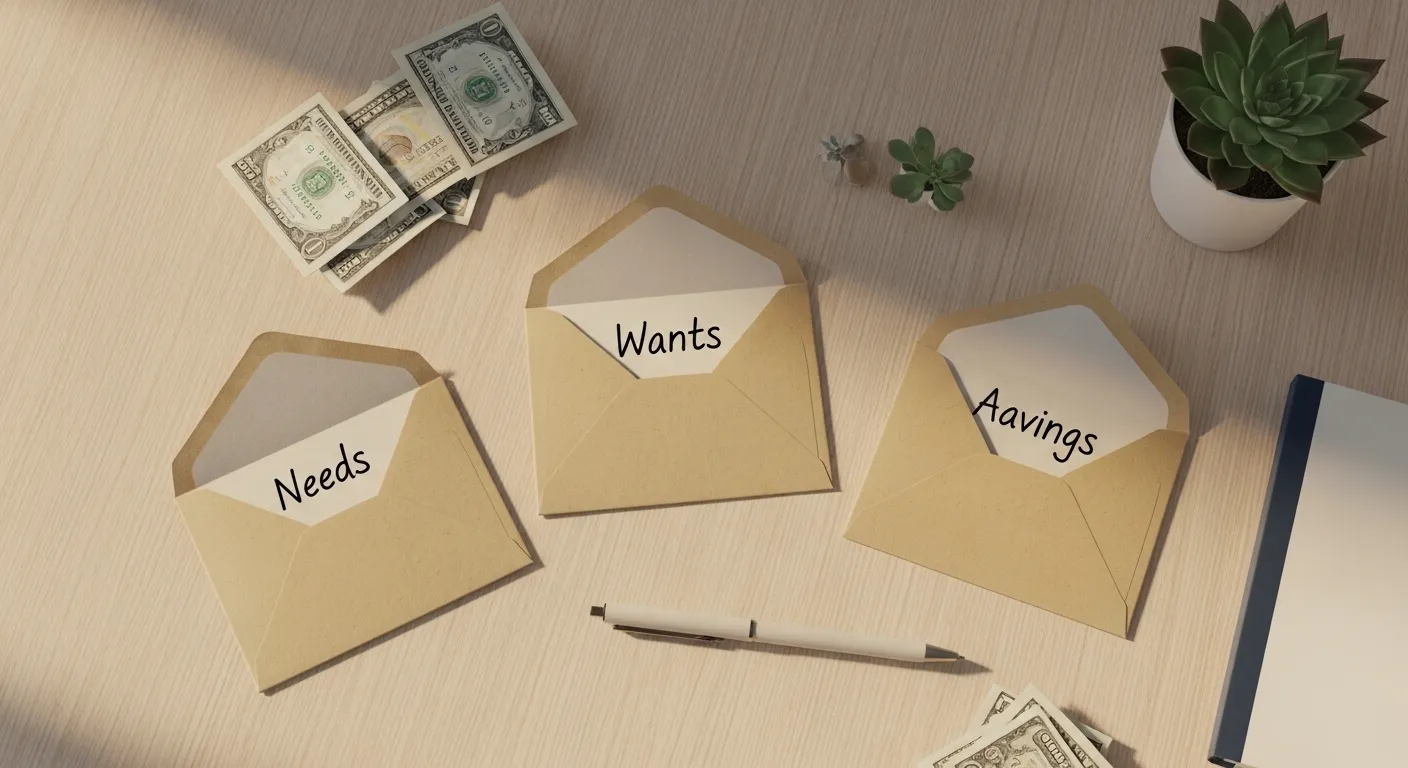

The 50/30/20 rule is a percentage-based budgeting framework popularised by U.S. Senator Elizabeth Warren in her book All Your Worth. It divides your monthly after-tax income into three simple buckets:

- <strong>50% Needs</strong> — rent, groceries, utilities, minimum debt payments, insurance

- <strong>30% Wants</strong> — dining out, streaming services, hobbies, travel

- <strong>20% Savings & Debt Repayment</strong> — emergency fund, retirement, extra debt payments

Step 1: Calculate Your After-Tax Income

Start with what actually lands in your bank account each month after taxes and payroll deductions. If you are salaried, this is straightforward. If you are freelance or self-employed, use your average net income from the last three months — and remember to set aside for taxes yourself.

Step 2: Assign the Percentages

Multiply your after-tax income by 0.50, 0.30, and 0.20 to get your three budget caps. For example, if you bring home $3,500 per month: Needs cap = $1,750 | Wants cap = $1,050 | Savings cap = $700.

Step 3: Track — But Keep It Simple

The rule works best when you check in weekly. You do not need to categorise every coffee purchase. Just log your spending in each of the three buckets. SpendScribe lets you create exactly three budget categories and see at a glance which bucket is running hot.

What If My Needs Exceed 50%?

In high cost-of-living cities, needs often run 60–65% of income. That is okay — treat it as a signal, not a failure. The goal is to work toward the 50% threshold over time by increasing income or reducing fixed costs like rent or car payments.

50/30/20 vs. Zero-Based Budgeting

Zero-based budgeting assigns every dollar a job, which is powerful but time-intensive. The 50/30/20 rule trades some precision for speed. Use 50/30/20 if you are new to budgeting or just want a quick sanity check. Graduate to zero-based once you have debt to attack or a specific savings goal.

Common Mistakes to Avoid

- Counting gross income instead of net income — always use take-home pay

- Putting subscriptions in Needs instead of Wants — streaming, gym, and music apps are Wants

- Forgetting irregular expenses like car registration, birthdays, or vet bills — smooth these into monthly averages

The 50/30/20 rule is not perfect, but it is the fastest way to go from no budget to a functioning one. Start this month, revisit in 30 days, and adjust. That simple habit compounds into real financial change.